Construction Cash Flow Management: A Practical Guide for Contractors

Free Download: Cash Flow Forecast Template

Cash flow management is not optional in a construction business. It is a core part of staying in business.

Between large receivables, slow-paying customers, progress billings, and significant payables to suppliers and subcontractors, cash moves in uneven ways. If you do not understand how to read your cash flow and anticipate what is coming next, you are effectively managing blind.

Unfortunately, most cash flow advice skips this step. Owners are told to invoice faster, tighten payment terms, or cut costs without first understanding what their cash flow is actually telling them.

You cannot fix a problem you have not clearly identified.

Before you can improve cash flow, you need to see where cash is being generated, where it is being tied up, and where it is leaking out of the business.

In this guide, I will walk through how to properly review your cash flow and how to build a simple, practical forecast so you can start planning ahead instead of reacting to cash shortages.

What is Cashflow Management?

Cash flow management is the process of actively planning, monitoring, and controlling how money moves in and out of your business.

It is not just about tracking what already happened. It is about making sure you have enough cash on hand to pay your people, suppliers, and bills when they are due, while still being able to fund ongoing work and growth.

In a construction business, this matters more than in most industries because cash timing is uneven.

You often pay for labour, materials, and subcontractors before you get paid by the client. Progress billings come later. Holdbacks delay a portion of your cash even longer. Change orders get approved after the work is already done. The result is that cash can leave your business weeks or months before it comes back in.

This is why cash flow management is not just about profit.

A job can be profitable on paper and still create cash pressure if the timing of payments does not line up with when expenses are due. Managing cash flow means understanding both the amount of cash moving through your business and the timing of those movements.

If you only look at your profit and loss statement, you miss half the picture.

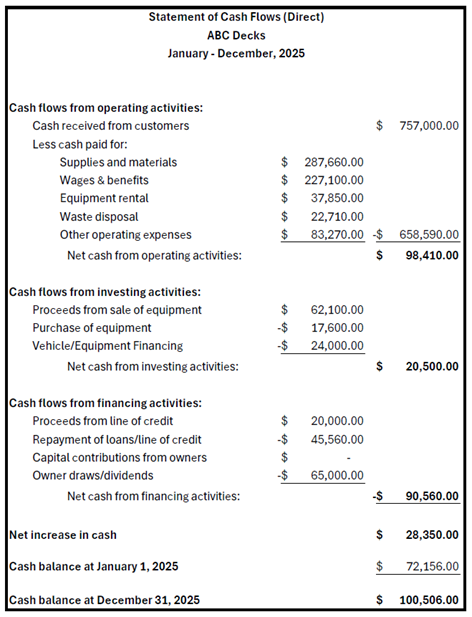

Example of a cash flow statement for a construction company. In the sections below, we’ll walk through what each part means and how to use it to manage your cash.

The Cashflow Management Process

Cash flow management is not a single report or a one-time exercise. It is a simple, repeatable process.

Step one is reviewing what already happened.

I start with the statement of cash flow. This shows how cash moved through the business across three areas: operating activities, investing activities, and financing activities. You do not need to be an accountant to get value from this report. The point is not perfection. The point is to build a basic understanding of where cash actually came from and where it went in the last period.

This gives you a baseline.

Without this step, you are guessing. You might feel “busy” or “profitable,” but you do not have a clear picture of whether the business itself is generating cash, or whether cash is only showing up because of loans, owner injections, or delayed payments.

Once you understand what already happened, you can move to the part that actually lets you manage cash: forecasting.

A cash flow forecast takes what you learned from your historical cash flow and projects it forward. It forces you to think about upcoming payroll, supplier payments, tax remittances, and expected customer payments before they happen. This is where cash flow management becomes proactive instead of reactive.

In simple terms:

First, review past cash flow to understand your reality.

Then, forecast future cash flow so you can plan your decisions.

This two-step loop is the core of cash flow management. Everything else is just a tactic layered on top of it.

How to Read Your Cash Flow Statement Without Being an Accountant

Most owners struggle with cash flow statements because they do not understand what the report is trying to show them.

A cash flow statement is simply a breakdown of how your cash changed over a period of time, grouped into three logical sources:

Operating activities

This section shows the cash generated or used by your actual day-to-day construction work.

• Customer payments

Progress billings, deposits, and final payments received from clients.

• Payroll and labour costs

Wages, payroll taxes, and subcontractor payments needed to complete jobs.

• Materials and supplier payments

Lumber, hardware, concrete, rentals, and other job-related purchases.

• Day-to-day overhead

Insurance, fuel, software, office expenses, and other operating costs.

This is the most important section of the entire report because it shows whether your core business operations are actually producing cash.

Investing activities

This section shows cash spent on long-term assets used to run and grow the business.

• Equipment purchases

Excavators, skid steers, compactors, and other heavy equipment.

• Vehicles and trailers

Work trucks, dump trailers, and transport equipment.

• Tools and shop equipment

Larger tool purchases or shop machinery used across multiple projects.

• Asset sales

Cash received from selling old vehicles, equipment, or tools.

These transactions affect cash, but they do not reflect day-to-day profitability. They represent investments in the future capacity of the business.

Financing activities

This section shows how the business raises cash or returns cash to owners and lenders.

• Loan proceeds

New financing from banks, equipment loans, or lines of credit.

• Loan repayments

Principal payments made on existing loans.

• Owner contributions

Cash injected by the owner to support the business.

• Owner draws or dividends

Cash taken out of the business by the owner.

This section explains how the business is funded, not whether the business itself is generating cash.

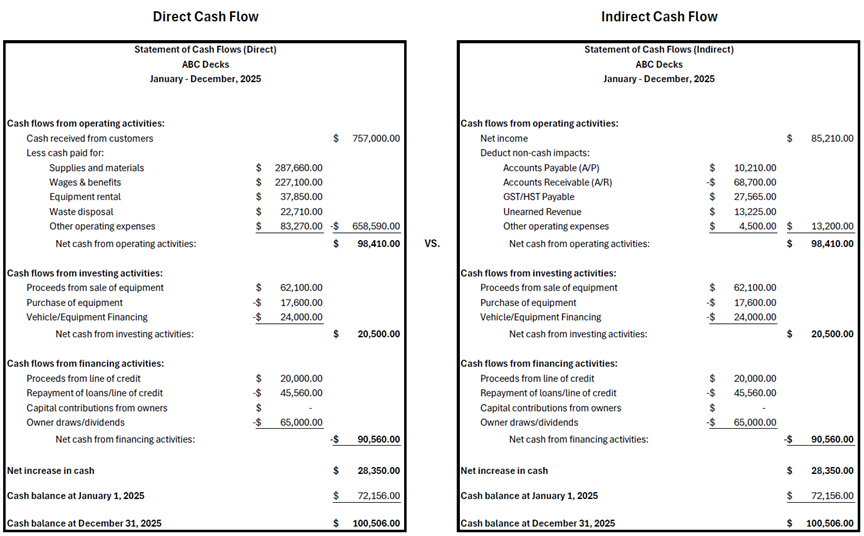

Direct vs indirect cash flow statements (why yours probably looks weird)

There are two ways a cash flow statement can be prepared: the direct method and indirect method.

A direct cash flow statement shows cash coming in and going out by category. For example, cash received from customers, cash paid to suppliers, and cash paid for payroll. This format is far more intuitive to read because it matches how owners actually think about money.

Most accounting systems, however, produce an indirect cash flow statement. Instead of listing cash inflows and outflows, it starts with profit and then adjusts for non-cash items to arrive at the same net cash result. The math is correct, but the presentation is much harder to interpret and far less useful for day-to-day understanding.

You can build a direct cash flow view manually, but that is outside the scope of this article.

I will include examples of both formats below so you can see the difference visually and understand why your cash flow statement probably looks more complicated than it needs to be but just remember that the subtotals of each section are exactly the same between the two methods.

A comparison of cash flow statement between the direct method and indirect method. Accounting systems by default produce indirect statements and are typically not as helpful as direct statements.

How to Build a Cash Flow Forecast You Can Actually Use

There are software tools that forecast cash flow but I still prefer good old fashioned Excel.

Not because it’s advanced, but because building it yourself forces you to understand your business.

Here’s exactly how to do it.

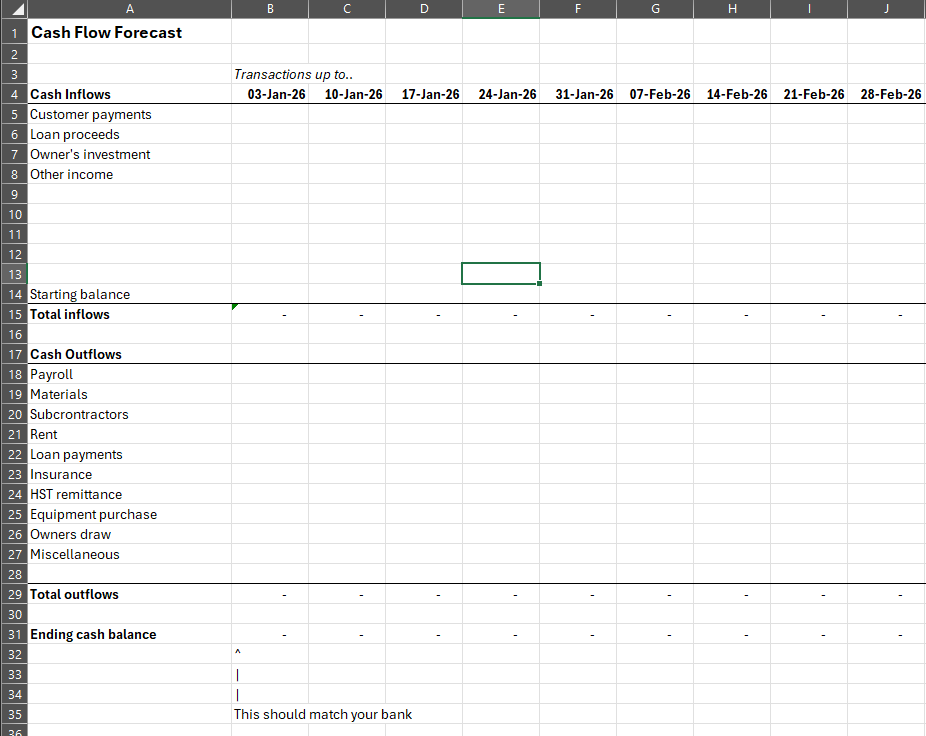

Step 1: Open a New Excel File and Build the Table

Click Here to Download the Forecasting Template

Open a blank Excel workbook.

In Column A, start listing categories.

At the top, add your cash inflows, for example:

Customer payments

Loan proceeds

Owner investment

Other income

Leave a blank row.

Then list your cash outflows, for example:

Payroll

Materials

Subcontractors

Rent

Loan payments

Insurance

HST remittances

Equipment purchases

Owner draws

Miscellaneous

Now move across the sheet.

Each column after Column A should represent one week.

Label them clearly at the top (for example: Week of Jan 6, Jan 13, Jan 20, etc.).

At the bottom of each weekly column:

Total inflows

Total outflows

Ending cash balance

This is your forecasting engine.

You can do daily or monthly columns, but for most construction businesses, weekly is the sweet spot. Monthly hides problems. Daily creates noise.

What your blank cash flow forecast should look like. Change up the categories to fit your business and needs.

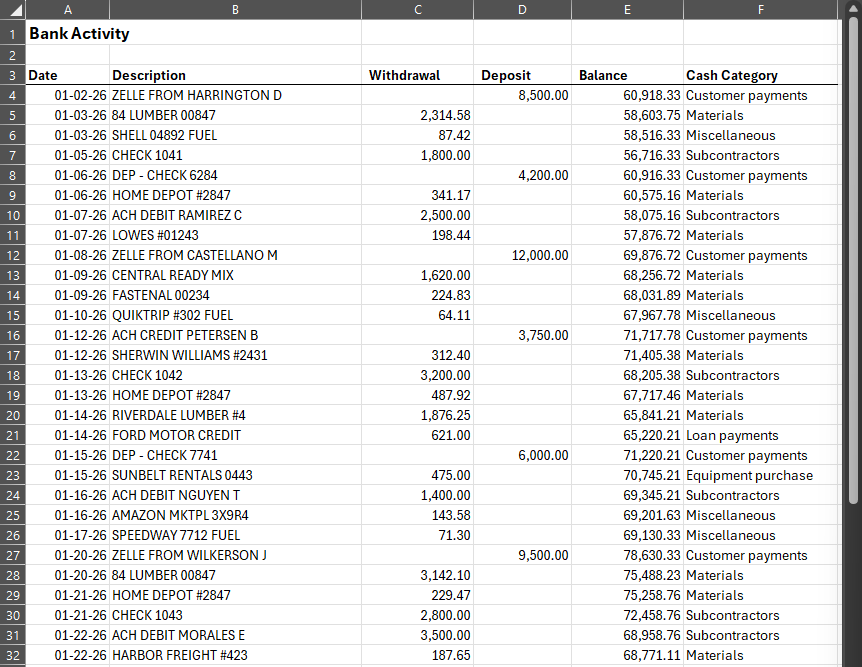

Step 2: Download 3 Months of Bank Transactions

An example bank activity file for our sample company ABC Decks

Go into your bank account and export the last 3 months of activity to Excel or CSV.

Now go line by line.

For each transaction:

Identify the week it occurred

Identify the correct category

Enter the amount in the matching cell

Yes, it’s manual.

No, it’s not busywork.

This forces you to:

See patterns in customer payment timing

Identify recurring overhead

Notice irregular spikes

Understand your true cash rhythm

Once finished, your table now shows three months of real cash history.

This is a one-time setup. After this, you simply update weekly.

Step 3: Continue Updating Weekly (Non-Negotiable)

At the end of every week:

Download that week’s transactions

Add them to the correct column

Review your ending cash balance

Cash flow forecasting only works if it becomes a habit.

If you only update it when you’re stressed, you’ve already lost control.

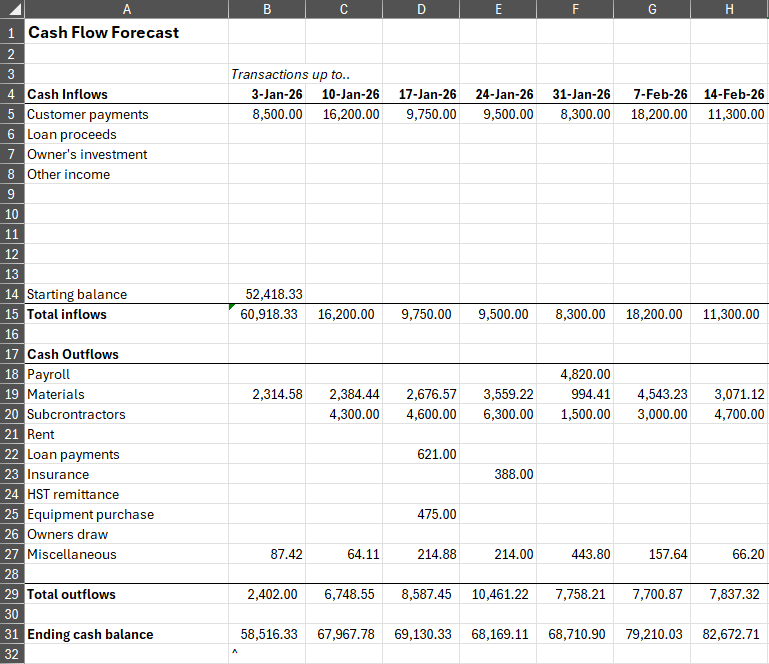

Our newly created cash flow forecast with each weeks transactions entered in

Step 4: Start Forecasting Future Weeks

Now extend your weekly columns forward.

Start by filling in the predictable items:

Fixed loan payments

Insurance

Rent

Software

Known tax deadlines

Then estimate the variable items:

Upcoming payroll

Materials for scheduled jobs

Subcontractor payouts

Expected customer payments

You can model this as precisely as you want.

But here’s the truth: the first 80% of clarity comes from rough but reasonable estimates. Trying to perfect the last 20% usually wastes time.

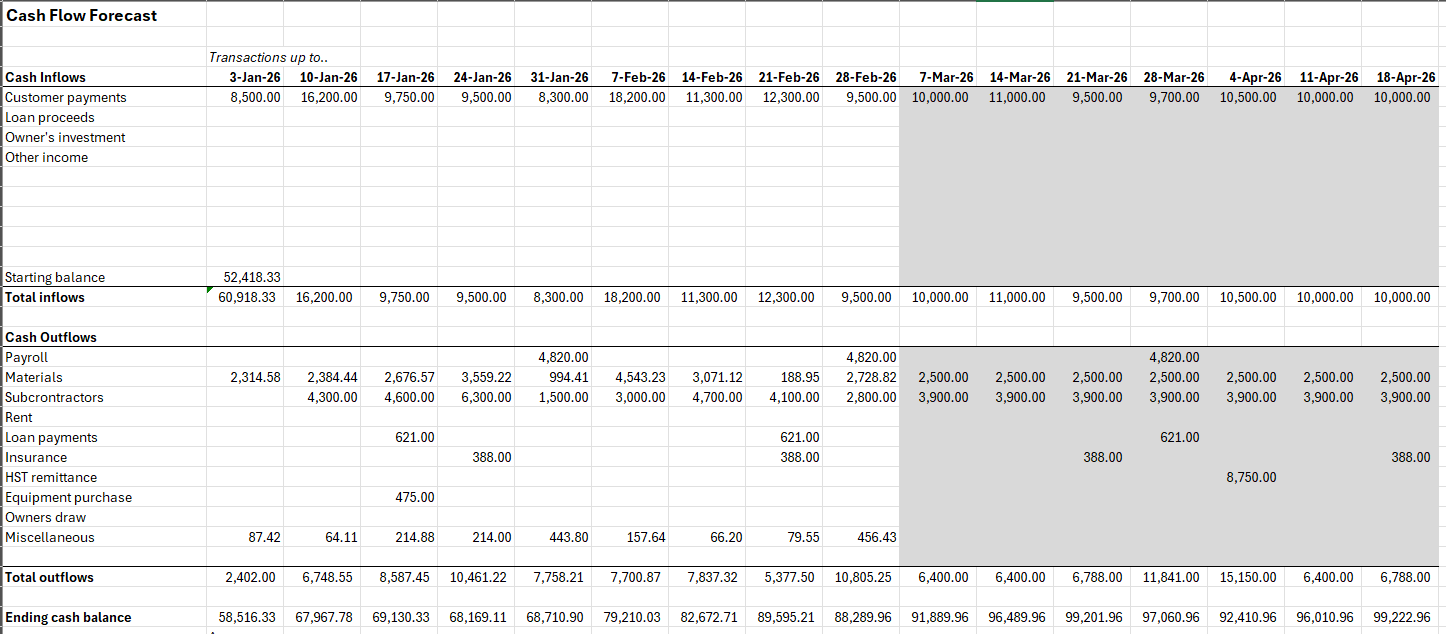

Our sample cash flow forecast with the future weeks entered in with our estimates. Once you do that, the fun part is to see how the business can deploy excess cash into either future growth or investment vehicles. Feel free to forecast as long a period as you’d like although 3, 6, 12 months are common.

Step 5: Use the Ending Balance to Make Decisions

Each future column will now show a projected ending cash balance.

This is where forecasting becomes powerful.

Now you can clearly see:

When cash dips

When you’ll be tight

When you’ll have surplus

Whether growth decisions are responsible

Instead of asking,

“Can we afford this?”

You’ll be asking,

“In which week does this decision create pressure?”

That’s a completely different level of control.

Want the Exact Template?

I’m put together the exact Excel template I use along with a step-by-step walkthrough video showing how to set it up and maintain it properly.

If you’d rather not build this from scratch, you’ll be able to download it and customize it for your business.

Use it consistently and cash flow stops being something that surprises you — and starts becoming something you manage intentionally.

Profit Isn’t Cash: Why Your P&L Can Look Fine While Your Bank Account Is Bleeding

Profit and cash are not the same thing.

Your P&L records revenue when you bill, not when you get paid.

It records expenses when they are incurred, not when the cash leaves your bank account.

This timing gap is where many growing construction businesses get stuck.

On paper, the business looks healthy. Jobs are profitable. Margins are solid.

But when it comes time to hire, buy equipment, or take on larger projects, everything suddenly feels uncertain.

Not because the business is unprofitable.

Because the cash is tied up.

Receivables can make revenue look strong while starving you of usable cash.

Long payment cycles and holdbacks delay when profit actually turns into money you can spend.

This leads to two common problems:

You think you can afford to grow, but your cash position cannot support it.

Or you hold back on smart growth because you do not trust your numbers.

Both slow your business down.

If you treat profit and cash as the same thing, you will keep making decisions that look right on your P&L and still feel risky in real life.

The Three Ways to Look at Cash Flow in a Growing Construction Company

Looking at a single bank balance does not tell you much about how healthy your cash flow really is.

Growing construction businesses need to look at cash flow from three different angles. Each one answers a different question. Miss one, and you end up making decisions with blind spots.

1. Business-level cash flow

This is the big-picture view of the company.

It answers one simple question:

Is the business, as a whole, generating cash or consuming it over time?

This view comes from your statement of cash flow. It shows how cash has moved through the business in recent periods and whether the company is actually funding itself or quietly relying on credit, owner injections, or delayed payments.

If business-level cash flow is weak, growth usually makes the problem worse, not better.

2. Job-level cash flow

Each project has its own cash reality.

This view answers the uncomfortable question:

Is this job funding itself, or is it being financed by your bank account?

Most basic bookkeeping systems do not show job-level cash flow clearly. You typically have to build this view yourself by mapping job billings and job costs over time, which is something that can be done very effectively in a simple cash flow forecast spreadsheet.

This is where you start to see which jobs feel “heavy” on cash and which ones are easier to carry, regardless of what the margins look like.

3. Forward-looking cash flow

This is the planning view.

It answers the question that drives real decisions:

Can I afford to hire, buy equipment, or take on more work without stressing the business?

This view comes directly from your cash flow forecast. It lines up expected cash coming in with known cash going out so you can see pressure points before they hit. This is what turns cash flow from something you react to into something you can actually manage.

How to Tell If Cash Flow Issues Are Structural or Just a Temporary Squeeze

I’m going to assume something about you.

You’re not running a failing company.

You’re likely profitable.

You’re busy.

You’re investing back into growth.

Growth consumes cash.

So even strong companies can feel tight.

When that happens, the real question is:

Are we temporarily tight because of timing and growth…

or is something fundamentally broken?

First Step: Look at Cash Flow From Operations

Open your cash flow statement.

Go directly to Cash Flow From Operating Activities.

This number answers one simple question:

Is your core business generating cash on its own?

Ignore loans. Ignore equipment purchases. Ignore owner contributions.

Just focus on operations.

Now ask:

Has operating cash flow been positive over the last 6–12 months?

Or has it been consistently negative?

If it’s positive over time, your model likely works.

If it’s negative over time, you likely have a structural issue.

That’s your first high-level filter.

What a Temporary Cash Squeeze Actually Looks Like

Now let’s make this practical.

A temporary squeeze usually has these characteristics:

1. You Can Point to a Specific Cause

For example:

“We just bought a truck.”

“We hired two employees before their revenue kicked in.”

“We front-loaded materials for a large project.”

“Two big invoices haven’t been paid yet.”

There’s a clear explanation for the dip.

2. You Have Invoices That Will Cover the Gap

Open your Accounts Receivable aging.

Ask:

Are the unpaid invoices tied to completed or nearly completed jobs?

Are they within normal payment terms?

Have these customers paid reliably in the past?

If yes, then the cash problem is likely timing. When those payments arrive, pressure should ease.

3. When Cash Comes In, Things Stabilize

This is the simplest test.

When customer payments hit:

Does stress drop?

Does the bank balance recover?

Does the problem temporarily disappear?

If yes, you likely have a timing mismatch.

That’s a working capital issue — not a broken business.

What a Structural Problem Looks Like

Structural issues feel different.

You’ll notice:

Even after major payments come in, you’re still tight.

Operating cash flow is negative across multiple quarters.

Revenue is growing, but bank balances aren’t.

You rely on debt just to fund normal payroll.

Margins are inconsistent or shrinking.

This tells you something deeper is wrong.

Common root causes:

Underpricing jobs.

Poor job costing.

Excessive overhead.

Growth without sufficient margin.

Chronic underbilling.

Here’s the key distinction:

If customer payments don’t meaningfully relieve the pressure,

you’re not dealing with timing.

You’re dealing with structure.

Why Cash Flow Matters for Growing Construction Companies

Healthy companies can absolutely experience cash stress, especially when aggressively reinvesting.

But healthy companies generate positive operating cash over time.

That’s your anchor.

Growth consumes cash.

Bad margins destroy cash.

Those are two very different problems.

Before reacting emotionally, borrow money, or slash expenses, take a step back and answer:

When the cash cycle completes… does the pressure disappear?

If yes: tighten systems.

If no: revisit pricing, margins, and cost structure.

That’s the difference between managing growth… and masking a deeper issue.